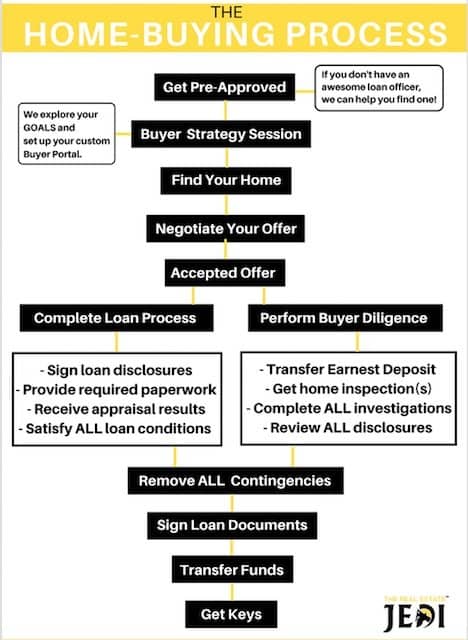

1.Opening Escrow

Typically, within a day or two of realizing an accepted purchase agreement, the parties will “open escrow,” This means that a copy of the fully-executed purchase agreement and associated documents are sent to the agreed-upon escrow company and the escrow officer opens a new transaction file.

2.Deposit EMD

Within 72 hours of offer acceptance (unless it falls on a weekend or is agreed otherwise) the buyer must deposit the agreed EMD amount into escrow where it will be held for the duration of the transaction.

3.Contingency Time-Frames

Contingency periods are time frames in which the buyer may further investigate matters pertaining to the purchase, prior to being 100 percent obligated to consummate the transaction.

a. Property Investigations

Unless agreed upon otherwise, the buyer has 17 days to conduct all buyer investigations, review all seller disclosures*, conduct inspections (whole-home inspection, pool inspection, roof inspection, foundation inspection, etc.) and any other research.

*Disclosures: It is the legal duty of the seller to disclose any known material facts to the buyer, as well as several other required statutory disclosures and supplemental forms.

b. Loan

Unless agreed upon differently, the buyer has 21 days to obtain full loan approval and to remove the loan contingency or cancel the deal.

Note: It is extremely important that you don’t make any changes to your employment or finances during escrow. The lender will pull your credit once more before closing and, if there are changes to your finances or employment, you may lose the loan approval and the home.

c. Appraisal

Unless agreed on differently, the buyer has 17 days by default to remove the appraisal contingency. If the appraisal comes in low (the appraiser claims the home is worth less than you offered), the buyer may attempt to re-negotiate the price with the seller or make up the difference between the appraised value and the purchase price with his or her own money.

If no agreement can be made, as long as the buyer has not removed this contingency, the buyer may cancel the deal, with a full return of his or her earnest money deposit.

d. Other Types

There are additional types of contingencies allowed — not just for the buyer but the seller as well. These are negotiable terms and may be added to the purchase agreement if agreed to by both parties.

Note: As long as the buyer has not removed the associated contingency, he or she has the right to cancel the deal and [typically] have the entire EMD refunded, minus any costs incurred by the seller as agreed on in the purchase contract.

4. Loan docs (…almost there)

The loan documents are what bring the entire loan together — they are the official agreement to the terms to which you agreed and when you sign them you will also be asked to sign the promissory note, agreeing to the terms of the loan.

5. Funding (WOO-HOO!!)

Once loan docs have been signed and submitted to the lender and escrow for final review and approval, the final conditions have been satisfied and signed off, your loan will be placed in line for funding.

We will give you the good news when your loan has funded.

6. Recording (last step)

The final step in the purchase process is when the deed is recorded at the County Recorder’s office. This process is final when the title company representative utters the three sweetest words a buyer and his or her agent can hear: “We’re on record!” You’ll be handed the keys to your new home. Congratulations!

Making the Move

You did it — you’re a homeowner now! Next comes the job of coordinating movers, packing and handling a change of address — all of it a delicate balancing act that requires attention to detail. We’re happy to help with this too ― check out our moving guide HERE!