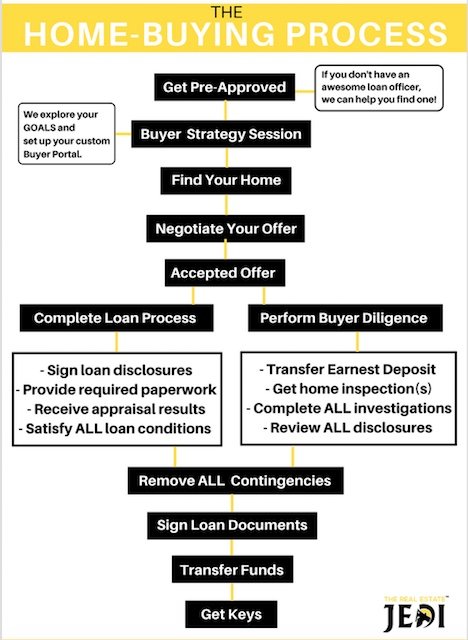

Learn the steps necessary to get on the path to owning real estate, and discover some helpful tips and tools along the way!

Detached Single-Family House

- No shared walls, floors or ceiling.

- Exclusive ownership of the land the house sits on (typically).

- Often higher-budget than comparable condos with similar characteristics.

Condominium

- An individual unit within a complex/community in which the owner owns only the interior of the unit.

- Ownership and responsibilities for the exterior and common areas are shared among homeowners.

Tip: Homeowner Association fees will play a part in your Debt-to-Income ratio (DTI), so it’s important to keep these fees in mind when considering your budget.

Multi-Family

- Residential properties with two to four units.

- Includes Duplexes, Triplexes and Fourplexes.

- Could also be 2-4 separate houses on one parcel.

- The owner owns all of the units collectively.

Note: May be financed with most traditional owner-occupied financing as long as buyer/borrower lives in one of the units.

1. Check the crime statistics for the area: A good place to start is online, at bestplaces.net. Here, you’ll be able to research tons of information such as the unemployment rates, education expenditures, crime rates, and where the community ranks in terms of a number of criteria.2. How are the neighborhood’s schools doing? It’s a fact that homes near a quality school hold their value better than homes near poor-performing schools. Get information on a neighborhood’s schools online at schooldigger.com and greatschools.org. Both provide access to proficiency ratings and more for local schools.

3. If you’re buying a rental property or want to check rental rates in the area, check out rentometer.com where you can enter an address and research the rents of the surrounding properties.Tip: Drive through desired neighborhoods during different times of the day and evening and on weekdays and weekends.

Head to work early one day and drive there from the neighborhood to get an idea of the traffic in the area.

This document is a thumbs-up from a lender indicating that you are eligible for a specified loan amount at a specified interest rate based on your documented income, assets, liabilities and credit score that you provided to the loan officer.

It informs you of the maximum amount you can borrow. This is vital information for a number of reasons. First, it gives you a home-buying budget so you won’t waste time looking at homes out of your price range. Next, a pre-approval letter impresses home sellers – it shows them you are serious about buying a home and the fact that you’ve started the loan process means a more streamlined escrow process.

Debt-To-Income Ratio (DTI)

The ratio of your total monthly financial obligations to your gross income is known in lending circles as your “debt-to-income ratio, or DTI for short. It plays a big role determining your maximum loan amount.

For example, if you have a salary of $10,000 per month before taxes, and your monthly debt payments (such as car payments, mortgage and other loan payments, child support and alimony payments, etc.) total $4,000, your DTI would be 40 percent. ($4,000/$10,000 = 0.4). Most lenders require that your DTI be 40 percent or less. This doesn’t mean you can’t get a mortgage if yours is higher, but you may have to pay a substantially higher interest rate or submit a larger down payment. It mostly depends on the strength of other information in your credit application

Payments

Your total monthly mortgage payment is comprised of four factors: principal, interest, taxes and insurance, or PITI for short. Your loan officer will provide you with an estimated total monthly payment to cover your loan.

Note: If your loan terms entail mortgage insurance, then you’ll need to include the amount into your monthly payment as well. This insurance is required by lenders (with the exception of Veterans Administration loans) when your down payment is less than 20 percent of the sales price of the home.

Types of Loan Programs

1.Conventional Loan: Down payments start as low as 3 percent for borrowers who plan to occupy the home and 20 percent second homes and investment purchases.

3. FHA Loan: Down payments start as low as 3.5 percent. A borrower may be eligible even with a FICO credit score of as low as 580, but it depends on the lender.

The FHA requires borrowers to pay monthly Mortgage Insurance Premiums (MIP) which serve as an insurance policy for the program. Unlike conventional loans in which the PMI is removed when the borrower achieves 20 percent equity in the home, FHA’s MPI remains for the life of the loan.

- Note: The condo complex “FHA-approved” status must be current on the HUD Portal.

2. Other Types: Special programs available from private lenders including hard money loans, foreign national loans and even investor cash flow loans and special programs for medical professionals (physicians, dentists and veterinarians).

4. VA Loan: This is a zero down payment program for active-duty military members, veterans and eligible widows and widowers.

- Note: A condo complex must be listed as “VA approved” on the Veterans Information Portal.

Your closing costs will be between 1 – 3% (of the purchase price) depending on the type of loan used.

The down payment isn’t the only cash-outlay you will incur when you purchase a home.

Everyone that works on your transaction needs to get paid, so expect to pay for a notary, the appraisal, the title company fee and more. These are known as “closing costs,” and the amount varies, depending on the transaction.

Your lender will send you an estimate after you are approved for the loan and then, using the same form, you will receive the final amount you will owe at closing.

Enough of that boring stuff— HERE’s where the fun begins!

By this point, you should have:

- Been pre-approved for a mortgage

- Determined your personal budget

- Chosen your desired neighborhood(s) and the type of property you want to buy

All set? Then it’s time to start viewing homes for sale!

You will be receiving email notifications the second a property meeting your criteria hits the market.

Once you have found properties that you would like to view in person, simply email, text or call usnand we will schedule the showings.

Ideally, if there are multiple properties in one area that you would like to view, then we will try to schedule them all during the same trip.

Popular neighborhoods, which are typically in high demand also generally have a low inventory of available homes so when a new listing pops up that matches your criteria with low inventory, when a new listing has we’ll arrange a showing as soon as possible.

Important Note: Especially in markets with high buyer demand and low supply, to have the best chance of getting your offer accepted, you will want to be prompt in viewing the property and submitting an offer.

The Purchase Agreement — the foundation of which is the “Offer”— is the first and one of the most important documents you will deal with when purchasing a home.

1. Price

While offering price is only one of many items in the purchase agreement that will make or break a deal, in most situations it is the most substantial item.

You’ll of course want to ensure you are not over-paying for the property — not only to ensure you don’t pay more than you need to — but also to ensure there will not be appraisal issues. We will research comparable sold properties (“comps”) to determine if the price you intend to offer is fair.

Keep in mind: The market is dictated by supply and demand, so if there are competing buyers, and you truly want the home, you may have to offer more than if it were a slower market.

2.EMD

The earnest money deposit is a standard, good-faith deposit demonstrating to the seller that you “earnestly intend to buy their property,” as long as you are still satisfied with it after your investigation period. The amount should typically be at least 1 percent of the offer price, and may be increased to instill more confidence in your offer.

3. Close of Escrow (“COE”)

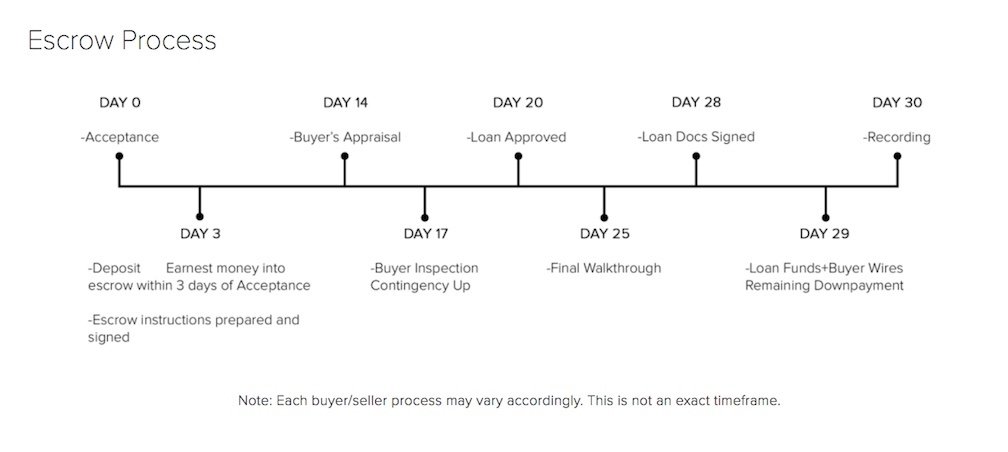

When would you like to close the transaction and get the keys? Typical time-frames for the length of escrow — from an accepted offer to closing the deal — vary and are negotiable, although 30 days is typical in the San Diego real estate market.

Before determining your desired closing date ensure that you’ve allowed sufficient time for completing your investigations and given your lender sufficient time to finish the loan.

4. Contingencies

By default, on the California Association of Realtors RPA form (the offer) the buyer is provided 17 days for property investigation contingencies, and 21 days for loan approval contingencies. This means that during those timelines, provided the buyer has not removed the contingencies, the buyer may cancel the deal for any reason provided for by existing contingencies and receive a full EMD refund.

5.Offer Acceptance

Once the buyer and seller have come to a mutual and complete agreement, they are said to have reached a “binding agreement.” This begins the transactional process known in California as “escrow”!

1.Opening Escrow

Typically, within a day or two of realizing an accepted purchase agreement, the parties will “open escrow,” This means that a copy of the fully-executed purchase agreement and associated documents are sent to the agreed-upon escrow company and the escrow officer opens a new transaction file.

2.Deposit EMD

Within 72 hours of offer acceptance (unless it falls on a weekend or is agreed otherwise) the buyer must deposit the agreed EMD amount into escrow where it will be held for the duration of the transaction.

3.Contingency Time-Frames

Contingency periods are time frames in which the buyer may further investigate matters pertaining to the purchase, prior to being 100 percent obligated to consummate the transaction.

a. Property Investigations

Unless agreed upon otherwise, the buyer has 17 days to conduct all buyer investigations, review all seller disclosures*, conduct inspections (whole-home inspection, pool inspection, roof inspection, foundation inspection, etc.) and any other research.

*Disclosures: It is the legal duty of the seller to disclose any known material facts to the buyer, as well as several other required statutory disclosures and supplemental forms. (Summary attached)

b. Loan

Unless agreed upon differently, the buyer has 21 days to obtain full loan approval and to remove the loan contingency or cancel the deal.

Note: It is extremely important that you don’t make any changes to your employment or finances during escrow. The lender will pull your credit once more before closing and, if there are changes to your finances or employment, you may lose the loan approval and the home.

c. Appraisal

Unless agreed on differently, the buyer has 17 days by default to remove the appraisal contingency. If the appraisal comes in low (the appraiser claims the home is worth less than you offered), the buyer may attempt to re-negotiate the price with the seller or make up the difference between the appraised value and the purchase price with his or her own money.

If no agreement can be made, as long as the buyer has not removed this contingency, the buyer may cancel the deal, with a full return of his or her earnest money deposit.

d. Other Types

There are additional types of contingencies allowed — not just for the buyer but the seller as well. These are negotiable terms and may be added to the purchase agreement if agreed to by both parties.

Note: As long as the buyer has not removed the associated contingency, he or she has the right to cancel the deal and [typically] have the entire EMD refunded, minus any costs incurred by the seller as agreed on in the purchase contract.

4. Loan docs (…almost there)

The loan documents are what bring the entire loan together — they are the official agreement to the terms to which you agreed and when you sign them you will also be asked to sign the promissory note, agreeing to the terms of the loan.

5. Funding (WOO-HOO!!)

Once loan docs have been signed and submitted to the lender and escrow for final review and approval, the final conditions have been satisfied and signed off, your loan will be placed in line for funding.

We will give you the good news when your loan has funded.

6. Recording (last step)

The final step in the purchase process is when the deed is recorded at the County Recorder’s office. This process is final when the title company representative utters the three sweetest words a buyer and his or her agent can hear: “We’re on record!” You’ll be handed the keys to your new home. Congratulations!

Making the Move

You did it — you’re a homeowner now! Next comes the job of coordinating movers, packing and handling a change of address — all of it a delicate balancing act that requires attention to detail. We’re happy to help with this too ― check out our moving guide HERE!