Many factors influence the value of your home. When it’s time to set a price, here are the main ones we look at:

Location

A neighborhood’s desirability is one of the biggest factors to determine a property’s value.

Competition

Buyers compare your property against others in that neighborhood. Available inventory will determine the demand for your property.

Condition

The property condition will affect price and speed of sale. Optimizing its physical appearance and condition will help maximize your property value.

The number one reason a home doesn’t sell in real estate is because the property is incorrectly priced.

By pricing your property at its true market value from the beginning, you will expose it to a much greater percentage of prospective buyers.

Keep in mind:

A property attracts the most attention, excitement and interest from the real estate community and potential buyers when it is first listed on the MLS.

We will give you up-to-date information on what is happening in the marketplace and the price, financing, terms and condition of competing properties. These are key factors in getting your property sold at the best price, quickly and with minimum hassle.

https://www.jedihomefinder.com/home-valuationWhat is a CMA ?

A comparative market analysis (CMA) is a detailed report that compares homes near you that have sold in recent months.

This is because a home is worth what a willing buyer will pay for it. Homes currently on the market are priced at what the seller hopes to get.

Sold homes, on the other hand, show us what buyers are actually willing to pay.

The goal is to find homes in your immediate area that are most similar to yours, analyze how quickly they sold and for how much.

This enables us to more accurately predict what other buyers will be willing to pay for your home.

What is Appraised Value?

An appraiser determines the estimated value of a property and is hired by the buyer’s lender to ensure that you haven’t offered the seller more than the home’s value and that the home complies with the minimal livability guidelines for loans.

One of the contingencies of the buyer’s offer is the appraisal. The lender will only loan you an amount of money up to the home’s current appraised value. This is why it’s so vital to price your home appropriately.

Note: Any repairs listed in the appraisal report as “required” ARE a condition of the sale.

From curb appeal to decluttering, make a commitment to focus on maximizing your home’s marketability.The number one reason a home doesn’t sell in real estate is because the property is incorrectly priced.

Have a pre-sale home inspection

A qualified and experienced home inspector will usually find something that should be corrected, upgraded, or repaired in every home that they inspect— even newly built homes!

Be pro-active and take care of these items; they will also show up on the buyer’s inspection, and if you wait until then you will lose valuable time. Remedying problems before the home is on the market also minimizes the likelihood that you will have a buyer back out of the deal because of the home inspection’s list of problems.

Tip: See “Top Home Inspection Findings” section.

The majority of these expenses are deducted from the sale proceeds – if you don’t sell, you don’t pay*

Note: we will provide you a Seller’s Estimated Net Proceeds worksheet with the estimated amounts for these fees.

*With the exception of performed services such as termite work or repairs.

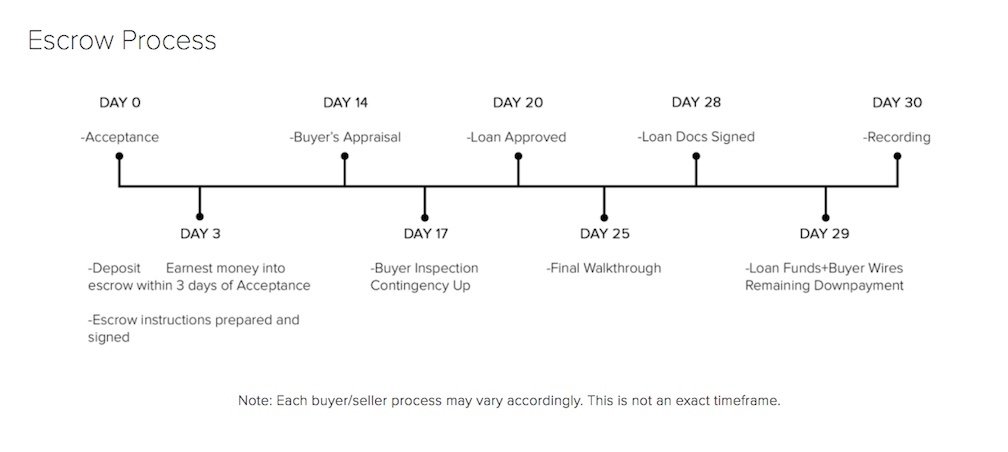

1. EMD: The buyer must transfer the earnest money deposit, in full, within 72 hours of acceptance of the offer (unless agreed otherwise).

3. Home inspection(s): The buyer should complete the home inspection and any other desired investigations within 17 days of acceptance. Please accommodate the buyer’s and the inspector’s schedules.

2. Seller’s Disclosures: The seller must provide these to buyer within 7 days of accepting the offer.

4. Removal of all contingencies:* must be done within 21 days of acceptance — meaning that the buyer must have full loan approval by the lender, including the appraisal results, have the home inspection completed and have met all the conditions of any other contingencies.

*Contingencies: Time-frames in which the buyer may further investigate matters pertaining to the purchase, prior to being 100 percent obligated to move forward with the transaction. Some of the main buyer contingencies include:

- Appraisal: The home is appraised at purchase price.

- Loan: The buyer’s ability to obtain financing.

- Property condition: Buyer to be satisfied with property condition, inspections, permits, records, disclosures and any other buyer investigations.

- Sale of buyer’s property. (if applicable)

- Buyer’s acceptance of items in the HOA documents.

5. Signing docs: After the appraiser confirms that any required repairs are completed, the buyer’s lender can “clear for loan docs.” This means that the loan documents will be sent to the title company. At this point, and upon buyer’s removal of all contingencies, it’s imperative that you don’t procrastinate on getting the repairs done ASAP! (which is why we suggest you do them BEFORE putting the home on the market). Escrow willassign a notary to collect your signatures on final docs and deed.

6. Close of escrow: This occurs on the date the grant deed or other evidence of title is recorded at the County Recorder’s office. It is done according to the time-frames agreed to in the purchase agreement. Once the buyer’s lender reviews and approves signed loan documents, the transaction is cleared for funding. Once escrow has received the funds, the transaction is cleared to be recorded.

When we receive confirmation that we are on record, escrow is “closed” and YOUR PROPERTY IS OFFICIALLY SOLD!